Seasonal Demand Impact on Bitumen Markets: Rainy vs Dry Season Effects

Across Asia, Africa, the Middle East, and beyond, construction activity and road paving programs follow distinct seasonal rhythms shaped by rainfall, temperature, and government budget cycles.

Understanding these patterns is not just academic knowledge — it is a procurement edge. Buyers who align their purchasing strategy with seasonal demand curves consistently achieve better pricing, more reliable supply, and stronger negotiating positions than those who react to market conditions after the fact.

This guide breaks down exactly how rainy and dry seasons move bitumen demand, which regions are most affected, and when the optimal procurement windows open across key markets.

Why Seasonal Patterns Define Bitumen Pricing

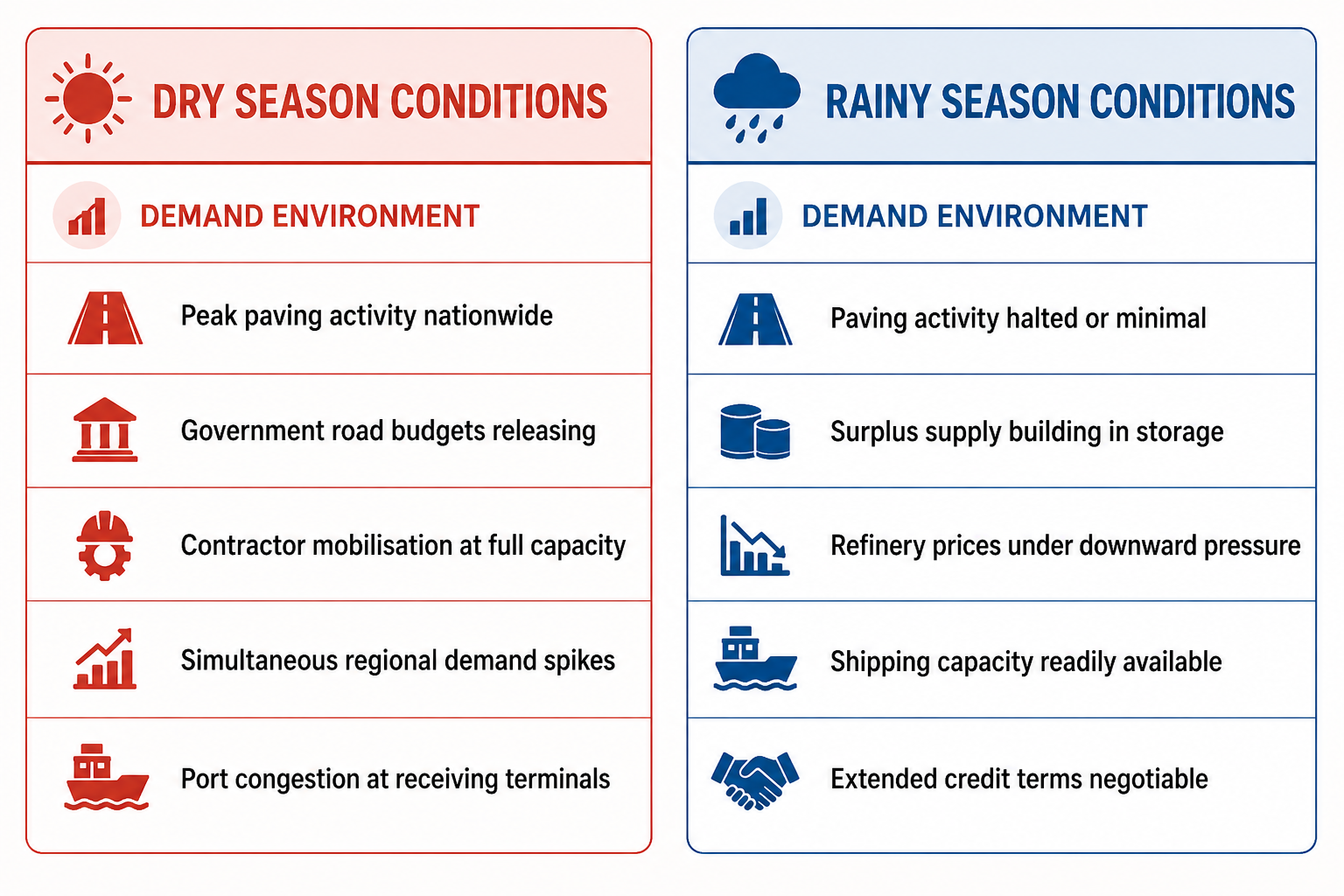

Bitumen is the binding agent in asphalt, making it indispensable for road construction, airport runways, and waterproofing applications. Unlike many commodities, bitumen demand is tightly coupled with weather conditions because asphalt cannot be laid effectively in wet weather. Rain compromises the bond between bitumen and aggregate, leading to premature pavement failure — so contractors simply stop paving when the rains arrive.

This creates a highly predictable demand calendar. Paving activity concentrates during dry periods, and procurement activity surges accordingly. Refineries and traders respond with tighter supply allocations, price premiums, and longer lead times. The buyers caught unprepared pay the peak price; the buyers who anticipated the cycle secure better terms.

The Dry Season Demand Surge

The dry season is the construction season. Government road agencies, private contractors, and infrastructure developers all converge on the same weather window, driving simultaneous demand spikes across entire regions. In Southeast Asia, this aligns with the October–April period. In sub-Saharan Africa, it varies by hemisphere — with West African markets peaking from November to March and East African markets from June to October. In South Asia, the post-monsoon window from October through March is the primary paving season.

Supply chain pressures during dry season

When dry season demand surges, supply chain stress follows. Shipping vessels book up, refinery run rates stretch toward capacity limits, and storage terminals at destination ports fill quickly. Importers who have not secured forward cargo positions face the double disadvantage of elevated spot prices and extended delivery lead times — sometimes stretching from the typical 2–3 weeks to 6 weeks or more during peak demand.

The Rainy Season Slow-Down — and Its Hidden Opportunity

The rainy season is when most bitumen buyers step back — and when the smartest ones step forward. With construction activity curtailed, demand for bitumen collapses across affected markets. Refineries continue producing, and supply accumulates. Sellers become motivated to move inventory, and the pricing dynamic reverses: buyers hold leverage they rarely enjoy during the dry season rush. Procurement teams that use the rainy season to negotiate forward contracts, lock in pricing for the upcoming dry season, and build strategic inventory are effectively buying their dry season supply at off-peak prices. Given that bitumen is a storable commodity — with shelf life typically ranging from 6 to 12 months depending on grade and storage conditions — this strategy is operationally viable for most buyers with adequate tankage.

Buyers who commit to volume during the rainy season, even at modest quantities, establish supplier relationships that translate into priority allocation and preferred pricing when peak demand returns. The rainy season is not downtime — it is a negotiating window.

The rainy season also presents an opportunity to align procurement with budget cycles. Many procurement teams operate on annual fiscal calendars that do not naturally sync with seasonal demand rhythms. Aligning budget releases with off-peak procurement windows requires internal planning discipline but delivers measurable savings on landed costs.

Market-by-Market Seasonal Calendar

Seasonality is not uniform. Each market has its own rainfall calendar, infrastructure program timing, and procurement behavior. The following overview covers the most significant bitumen-consuming regions and their seasonal demand cycles.

| Region / Market | Peak Demand Season | Off-Peak Season | Optimal Procurement Window |

| Southeast Asia Vietnam, Thailand, Indonesia |

Nov – Apr | Jun – Sep | Aug – Oct (pre-season stocking) |

| South Asia India, Bangladesh, Sri Lanka |

Oct – Mar | Jun – Sep | Jul – Sep (monsoon off-peak) |

| West Africa Ghana, Nigeria, Côte d’Ivoire |

Nov – Mar | May – Sep | Aug – Oct (pre-season forward buying) |

| East Africa Kenya, Tanzania, Ethiopia |

Jun – Oct | Mar – May | Jan – Mar (long rains pre-buying) |

| Middle East / Gulf Saudi Arabia, Yemen, Qatar |

Sep – May | Jun – Aug | Jun – Aug (summer heat pause) |

Note that the Gulf markets are an important exception to the rain-driven model. In these predominantly arid regions, it is summer heat rather than rainfall that interrupts construction. Extreme temperatures above 45°C make asphalt laying impractical from June through August, creating a distinct demand trough that mirrors the seasonal patterns seen in tropical markets — just driven by temperature rather than precipitation.

Optimal Procurement Timing Strategy

Translating seasonal awareness into a procurement strategy requires matching your buying timeline to market conditions rather than project timelines alone. The following principles apply across most markets.

Lock in supply 6–10 weeks before peak demand

Given shipping lead times from major producing regions — typically Iran, South Korea, Singapore, and the UAE — a 6 to 10 week forward horizon is the minimum required to secure dry season supply without paying a panic premium. This means procurement action in August and September for markets with November peak demand, and in June and July for markets peaking in October.

Use the off-peak season for contract negotiation

Even if physical delivery is not required during the rainy season, this is the ideal window for negotiating annual supply agreements, framework contracts, and pricing formulas. Sellers are more flexible on price basis, payment terms, and minimum order quantities when their order books are thinner. Buyers who establish these relationships during the off-peak season access preferential treatment when peak demand tightens availability.

Build strategic buffer stock where storage permits

For buyers with access to sufficient tankage, carrying 4 to 8 weeks of buffer stock entering peak season eliminates exposure to spot price spikes and supply disruptions. The carrying cost of this inventory is almost always lower than the premium paid on last-minute spot purchases at peak demand pricing. Storage costs typically run between 0.3–0.8% of cargo value per month — far less than the 10–15% price differential between seasonal low and seasonal high.

Track crude oil price trends alongside seasonal procurement planning. Bitumen is a crude derivative, and its refinery gate price moves with crude differentials. A rising crude environment entering peak demand season compounds the seasonal premium — doubling the motivation to buy forward. A falling crude environment may justify waiting, even during peak demand, if the price downtrend is strong enough.

Risk Factors That Distort Seasonal Patterns

While seasonal demand patterns are reliable, they are not immune to disruption. Buyers should account for the following variables that can shift or amplify expected seasonal dynamics.

Irregular rainfall patterns: Climate variability increasingly produces early or extended rainy seasons, compressing the paving window and creating sharper, more intense demand spikes when the dry season finally arrives. A short dry season with unchanged road programs means the same volume of bitumen is procured in less time — intensifying supply competition.

Government budget release timing: In many markets, road construction is heavily state-funded. Delays in budget approvals or late release of project tenders can shift peak demand by four to six weeks relative to the seasonal calendar. Monitoring government tender pipelines in target markets provides early warning of demand timing shifts.

Refinery outages and production disruptions: Supply shocks from refinery maintenance or geopolitical disruptions in producing countries — particularly Iran, which supplies a significant share of bitumen to Asian and African markets — can tighten availability independent of seasonal demand, pushing prices higher even during traditional off-peak windows.

Currency fluctuations: Bitumen is priced in US dollars across international trade. Currency depreciation in importing markets raises the effective local cost of bitumen, sometimes triggering demand destruction even during peak paving seasons, as road projects become unaffordable to execute at prevailing prices.

Bringing It All Together

The seasonal procurement framework

Bitumen markets reward buyers who plan ahead. The core principle is simple: procure during low demand, deliver ahead of peak demand, and never enter peak season exposed to spot markets. Use rainy seasons for contract negotiation and relationship building. Use the transition window — 6 to 10 weeks before peak demand — for physical cargo booking. Maintain buffer stock to absorb supply disruptions during peak season.

Applied consistently across procurement cycles, this approach reduces bitumen landed costs, improves supply reliability, and builds the kind of supplier relationships that matter most when everyone else is scrambling for cargo.

Frequently Asked Questions

Does the rainy season always mean lower bitumen prices?

Generally, yes — demand-driven pressure eases during rainy seasons, and motivated sellers often offer better terms. However, if a major supply disruption coincides with the rainy season, prices can remain elevated despite reduced demand. Monitor both demand and supply sides simultaneously.

How far ahead should procurement teams begin planning for peak season?

Ideally, the planning process begins 3 to 4 months ahead of anticipated peak demand, with contract negotiations starting in the off-peak window and physical cargo bookings confirmed 6 to 10 weeks before delivery is needed.

Are tropical markets the only ones affected by seasonal bitumen demand?

No. Temperate and arid markets also show strong seasonality — driven by winter in northern climates and summer heat in desert regions. The mechanism differs from rainfall-driven markets, but the procurement logic is identical: identify the demand trough and use it as your buying window.

Can small buyers benefit from seasonal procurement strategies?

Absolutely. Even buyers without large storage capacity can benefit by negotiating annual framework contracts during off-peak periods, locking in pricing formulas and priority allocation that apply during peak season deliveries.

Request a Seasonal Price Indication

Get CFR pricing for your discharge port with current availability — 60/70, 80/100, and VG grades.