Bitumen Market Overview 31 March 2026

Global Geopolitical Update

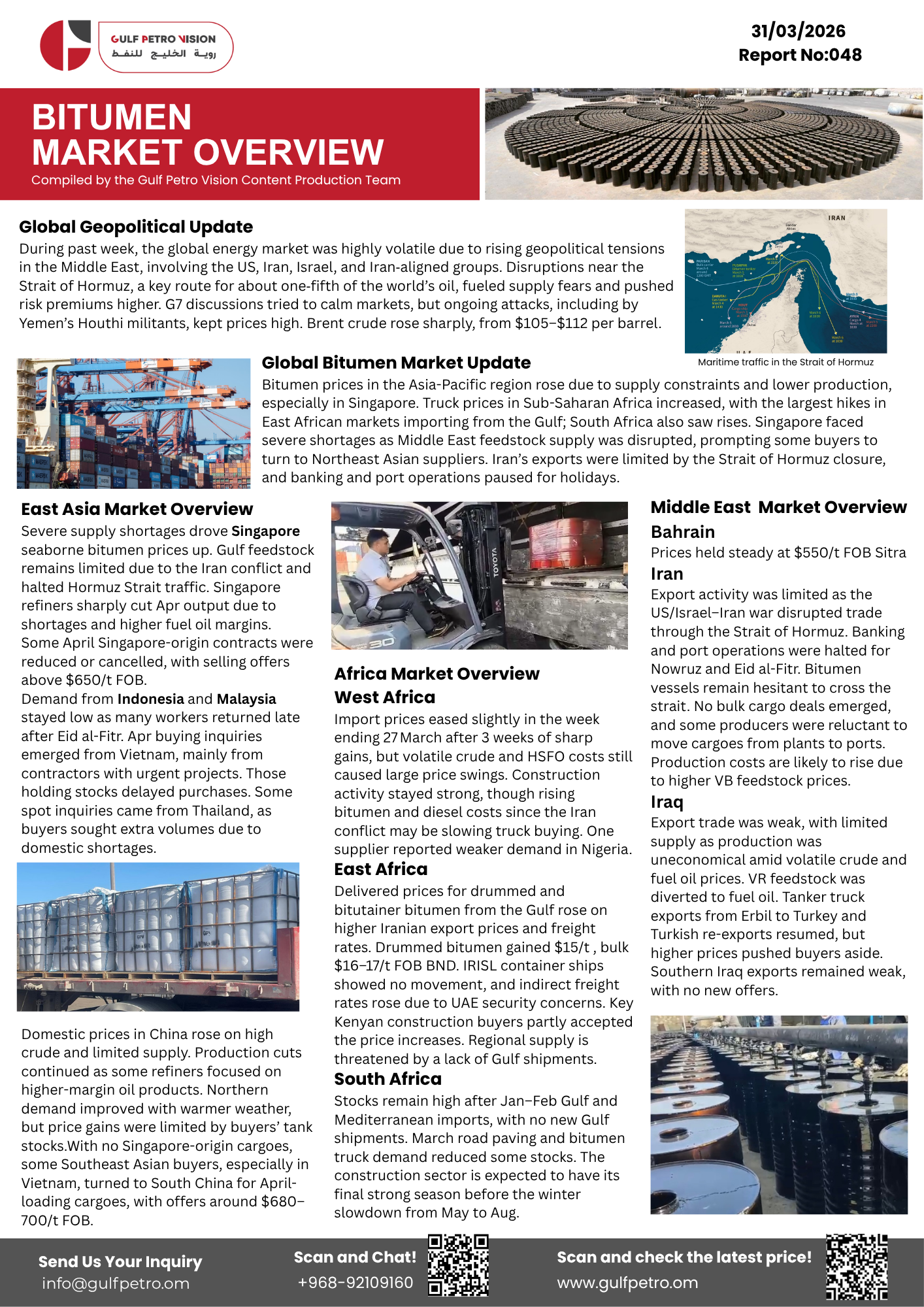

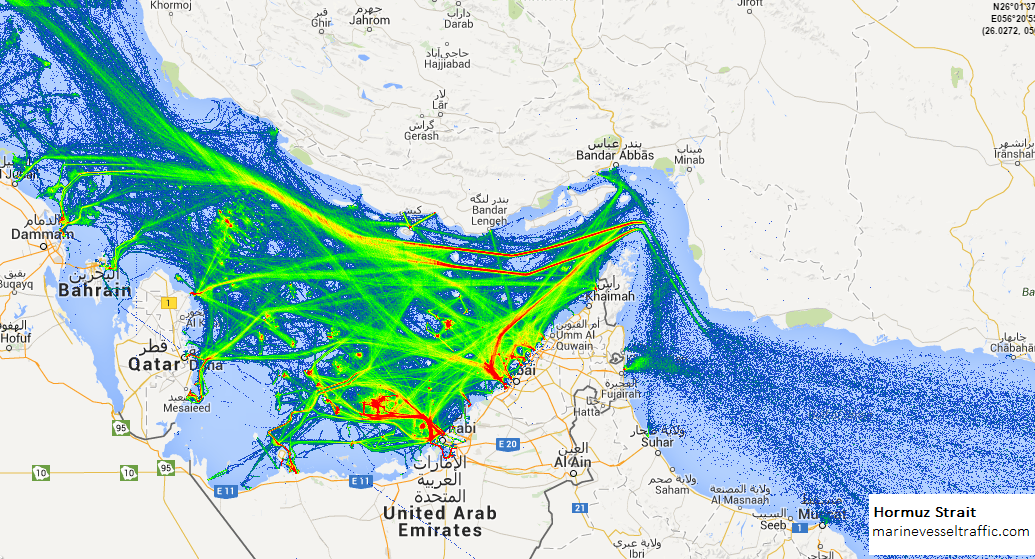

During past week, the global bitumen market update and energy market was highly volatile due to rising geopolitical tensions in the Middle East, involving the US, Iran, Israel, and Iran‑aligned groups. Disruptions near the Strait of Hormuz, a key route for about one‑fifth of the world’s oil, fueled supply fears and pushed risk premiums higher. G7 discussions tried to calm markets, but ongoing attacks, including by Yemen’s Houthi militants, kept prices high. Brent crude rose sharply, from $105–$112 per barrel.

Global Bitumen Market Update

Bitumen prices in the Asia-Pacific region rose due to supply constraints and lower production, especially in Singapore. Truck prices in Sub-Saharan Africa increased, with the largest hikes in East African global bitumen markets importing from the Gulf; South Africa also saw rises. Singapore faced severe shortages as Middle East feedstock supply was disrupted, prompting some buyers to turn to Northeast Asian suppliers. Iran’s exports were limited by the Strait of Hormuz closure, and banking and port operations paused for holidays.

East Asia Market Overview

Severe supply shortages drove Singapore seaborne bitumen prices up. Gulf feedstock remains limited due to the Iran conflict and halted Hormuz Strait traffic. Singapore refiners sharply cut Apr output due to shortages and higher fuel oil margins.

Some April Singapore-origin contracts were reduced or cancelled, with selling offers above $650/t FOB. Demand from Indonesia and Malaysia stayed low as many workers returned late after Eid al-Fitr. Apr buying inquiries emerged from Vietnam, mainly from contractors with urgent projects. Those holding stocks delayed purchases. Some spot inquiries came from Thailand, as buyers sought extra volumes due to domestic shortages.

Domestic prices in China rose on high crude and limited supply. Production cuts continued as some refiners focused on higher-margin oil products. Northern demand improved with warmer weather, but price gains were limited by buyers’ tank stocks with no Singapore-origin cargoes, some Southeast Asian buyers, especially in Vietnam, turned to South China for April-loading cargoes, with offers around $680–700/t FOB.

Africa Global Bitumen Market Overview

West Africa

Import prices eased slightly in the week ending 27 March after 3 weeks of sharp gains, but volatile crude and HSFO costs still caused large price swings. Construction activity stayed strong, though rising bitumen and diesel costs since the Iran conflict may be slowing truck buying. One supplier reported weaker demand in Nigeria.

East Africa

South Africa

Middle East Market Overview

Bahrain

Prices held steady at $550/t FOB Sitra.

Iran

Export activity was limited as the US/Israel–Iran war disrupted trade through the Strait of Hormuz. Banking and port operations were halted for Nowruz and Eid al-Fitr. Bitumen vessels remain hesitant to cross the strait. No bulk cargo deals emerged, and some producers were reluctant to move cargoes from plants to ports. Production costs are likely to rise due to higher VB feedstock prices.

Iraq

Export trade was weak, with limited supply as production was uneconomical amid volatile crude and fuel oil prices. VR feedstock was diverted to fuel oil. Tanker truck exports from Erbil to Turkey and Turkish re-exports resumed, but higher prices pushed buyers aside. Southern Iraq exports remained weak, with no new offers.