Bitumen Market Overview 21 April 2025

Crude Oil Price Fluctuations Driven by Global Factors

The crude oil and bitumen market trends were influenced by several global and regional factors. Globally, concerns about potential U.S. tariffs, fears of an economic recession, geopolitical tensions in the Middle East, and supply disruptions in the Gulf of Mexico drove market volatility. OPEC+’s decision to delay a planned production increase also affected pricing. In the second week of April 2025, Brent crude oil prices experienced significant fluctuations, falling below $60 per barrel amid trade tensions and oversupply concerns, before rebounding to around $65 as some tariff measures were postponed.

Global Bitumen Price Overview

Regionally, bitumen prices rose in Northeast Europe and the Mediterranean due to higher crude prices, while prices in Asia and the Gulf declined. Bahrain reduced its export price by $5, and Singapore’s prices dropped amid strong competition. Meanwhile, imports increased to Libya and South Africa, while East African prices fell, driven by lower Iranian bitumen prices.

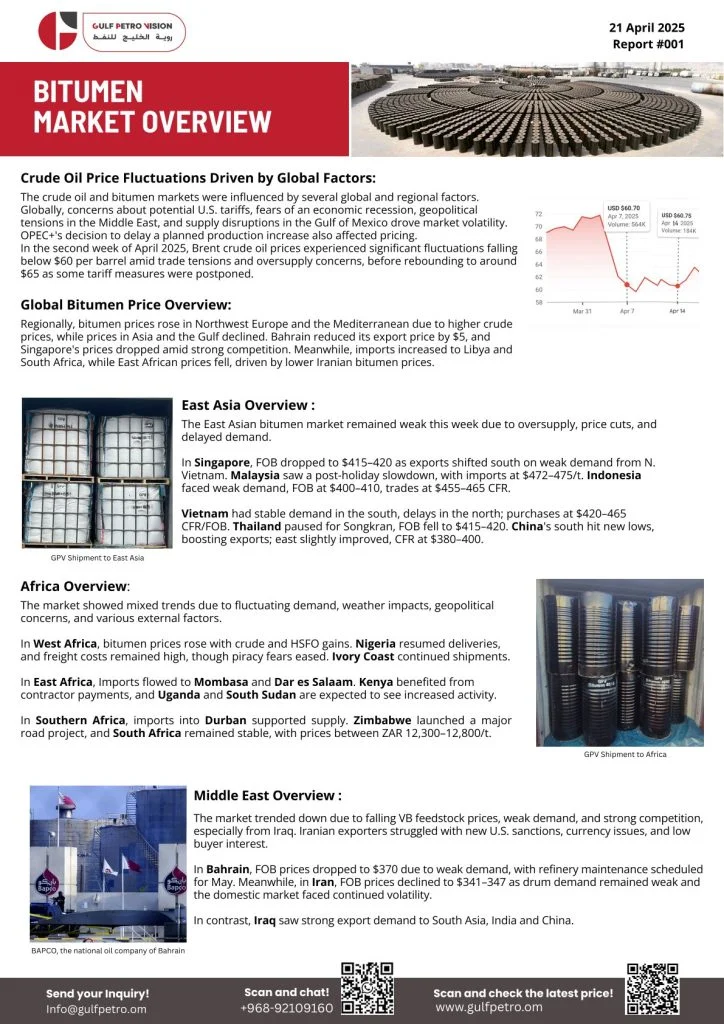

East Asia Market Overview

The East Asian bitumen market trends remained weak this week due to oversupply, price cuts, and delayed demand.

In Singapore, FOB dropped to $415-420 as exports shifted south on weak demand from N. Vietnam. Malaysia saw a post-holiday slowdown, with imports at $472-475/t. Indonesia local wet demand FOB at $400-410, trades at $405-407/t.

Vietnam had stable demand in the south, delays in the north purchases at $420-465 CFR/FOB. Thailand paused for Songkran, FOB fell to $415-420. China’s south hit new lows, boosting exports; east slightly improved, CFR at $380-400.

Africa Overview

The market showed mixed trends due to fluctuating demand, weather impacts, geopolitical concerns, and various external factors.

In West Africa, bitumen prices rose with crude and HSFO gains. Nigeria resumed deliveries, and freight costs remained high, though piracy fears eased. Ivory Coast continued shipments.

In East Africa, imports flowed to Mombasa and Dar es Salaam. Kenya benefited from contractor payments, and Uganda and South Sudan are expected to see increased activity.

In Southern Africa, imports into Durban supported supply. Zimbabwe launched a major road project, and South Africa remained stable, with prices between ZAR 12,300-12,800/t.

Middle East Overview

The market trended down due to falling VB feedstock prices, weak demand, and strong competition, especially from Iraq. Iranian exporters struggled with new U.S. sanctions, currency issues, and low buyer interest.

In Bahrain, FOB prices dropped to $370 due to weak demand, with refinery maintenance scheduled for May. Meanwhile, in Iran, FOB prices declined to $341-347 as drum demand remained weak and the domestic market faced continued volatility.

In contrast, Iraq saw strong export demand to South Asia, India, and China.